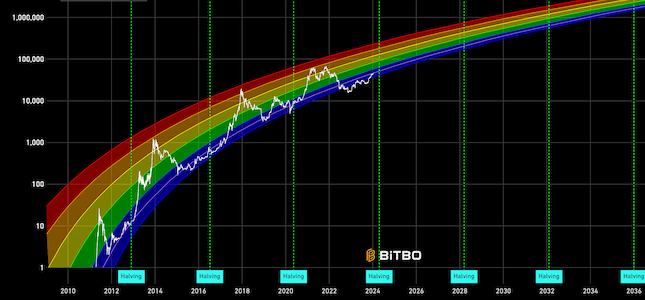

Bitcoin Rainbow Chart

A Bitcoin rainbow chart using only the halving dates as data.

Data & charts updated every hour

|

LeverageThe assumed leverage used by traders. Higher leverage means liquidations occur closer to the entry price.

|

RangeSets the minimum visible price range on the chart, centred on the current price. Useful for zooming in or out to see nearby liquidation clusters.

|

Margin RateThe maintenance margin rate required by the exchange before liquidation is triggered.

0.4%

|

Decay Rate (λ)Controls how quickly older candles lose influence.

0.2

|

For each hourly candle, the chart estimates the liquidation price for long and short positions opened at that candle's open price, weighted by trading volume and recency. The resulting pressure is bucketed into $250 price bands and displayed as a horizontal bar chart.

The liquidation price depends on the leverage level and the margin rate. For long positions, liquidation occurs when the price drops below the entry price by the inverse of the leverage ratio (adjusted for margin requirements). For short positions, liquidation triggers when the price rises above the entry price, calculated as follows:

Each candle's contribution is weighted by its trading volume and decay (λ) rate over time. This gives more weight to recent high-volume candles while reducing the influence of older candels. The decay rate (λ) controls how this influence, eg for the default λ = 0.2, a 5-hour-old candle retains about 37% of its weight, while a 24-hour-old candle retains only 8%, calculated by:

The weighted volume for each candle is split between long and short liquidation levels based on real-time traded long/short posistions, using the Binance api*. This creates separate accumulation patterns for upside (short liquidations) and downside (long liquidations) pressure:

*This chart uses Binance Futures API endpoints for real-time data.

A Bitcoin rainbow chart using only the halving dates as data.

Bitcoin's natural long-term power-law corridor of growth.

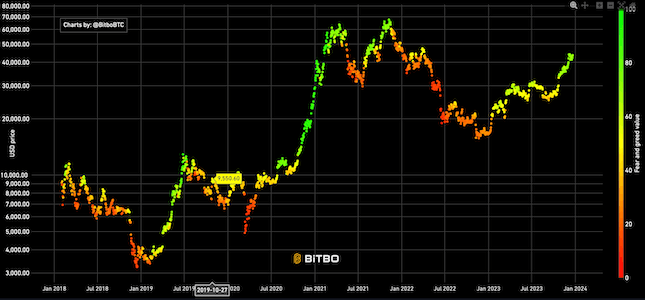

A sentiment analysis tool for Bitcoin and crypto markets, indicating when markets are overly fearful or greedy.

Bitbo's charts section offers a wide range of Bitcoin charts and metrics.

If you have any questions, comments, or feedback please reach out to us via Twitter or via email at info@bitbo.io.